This guide is for HR professionals, finance teams, business owners, and enterprises (including GCCs and product organizations) operating in India who need a practical grip on how payroll actually works — not just what it is. You'll learn the step-by-step payroll process, how salaries are calculated, key compliance obligations, and the most common mistakes companies make.

Key Takeaways

- Indian payroll runs on a three-phase monthly cycle: pre-payroll data collection, salary calculation, and post-payroll disbursement

- Net Pay = Gross Salary minus PF, ESI, Professional Tax, and TDS

- Employers must comply with central acts (EPF, ESI, Income Tax) and state-specific Professional Tax and minimum wage rules

- Late TDS deposits attract 1.5% monthly interest; late filings incur ₹200/day penalties under Section 234E

- Multi-state employers must navigate PT slabs, minimum wages, and Labour Welfare Fund thresholds that vary by state

What Is Payroll Processing in India?

Payroll processing is the structured monthly process through which an employer computes each employee's gross salary, applies statutory and voluntary deductions, calculates net pay, disburses salaries, and files required reports with government authorities. This cycle repeats every month and demands precision at every stage: from capturing attendance data to submitting quarterly TDS returns.

India's payroll system sits at the intersection of HR, finance, and compliance. It is governed by both central legislation (Income Tax Act, EPF Act) and state-level regulations (Professional Tax, Shops and Establishments Act), making it more layered than payroll in many other countries.

The Government of India consolidated 29 central labour laws into four Labour Codes, which became effective on November 21, 2025. Despite this consolidation, states like Karnataka, Maharashtra, and Kerala have notified their own rules, while others remain in draft, so employers still need a state-by-state compliance map.

Payroll processing vs. payroll management: Processing refers to the monthly calculation and disbursement cycle, while management encompasses the full-year activity including Form 16 issuance, year-end reconciliations, salary revisions, and handling exits/final settlements.

How Payroll Processing Works in India: A Step-by-Step Breakdown

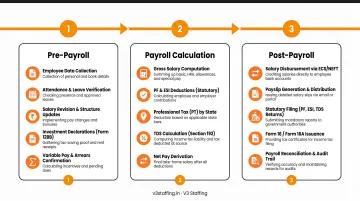

Payroll in India runs on a consistent monthly cycle with three sequential phases: pre-payroll, actual payroll calculation, and post-payroll. Each phase must be completed without errors before the next begins.

Pre-Payroll Activities

During the pre-payroll phase, teams collect and validate employee data (PAN, Aadhaar, bank details, salary structures), gather attendance and leave records, process expense reimbursements, and obtain investment declarations for tax estimation.

Validating inputs before calculation is critical. Errors in attendance data, LOP (Loss of Pay) adjustments, or investment declarations cascade into incorrect tax deductions that are difficult to reverse once processed.

For example, if an employee submits an updated 80C declaration mid-year but payroll doesn't reflect it, TDS will be over-deducted, creating reconciliation headaches at year-end.

Payroll Calculation

The actual calculation phase involves:

- Computing gross salary from the defined salary structure

- Applying leave deductions and arrears

- Estimating and deducting TDS based on projected annual income and declared investments

- Calculating contributions to PF, ESI, and Professional Tax

Simple illustrative formula:

- Gross Salary = Basic + HRA + Allowances + Bonuses + Reimbursements

- Net Salary = Gross Salary − (PF + ESI + PT + TDS + other deductions)

Example: An employee earning ₹50,000 gross (₹25,000 basic, ₹12,500 HRA, ₹12,500 special allowance) would have:

- PF deduction: 12% of ₹25,000 = ₹3,000

- ESI: Not applicable (gross exceeds ₹21,000/month)

- PT: ₹200 (assuming Karnataka state)

- TDS: Calculated based on annual income and regime choice

Net salary comes to approximately ₹46,800 after statutory deductions.

Post-Payroll Activities

Post-payroll includes:

- Transferring net salaries to employee bank accounts (typically via bulk NEFT transfers)

- Generating and distributing payslips

- Depositing statutory contributions: TDS by the 7th, PF and ESI by the 15th of the following month

- Filing quarterly/annual returns such as Form 24Q and Form 16

Beyond the recurring cycle, post-payroll handles ad hoc tasks: processing full-and-final settlements for exiting employees, managing arrear payments after salary revisions, and updating records after mid-year tax declaration changes.

How Salary Is Calculated in India: Key Payroll Components

Understanding CTC (Cost to Company)

CTC is the total annual expenditure an employer incurs on an employee: basic salary, all allowances, statutory contributions (employer-side PF, ESI), gratuity provisioning, and any perquisites. It is not the employee's take-home amount — the gap between CTC and in-hand salary is often larger than employees expect.

Earnings Components

Basic Salary: Typically 40–50% of CTC, fully taxable, and forms the base for PF and gratuity calculations. PF contributions are calculated on Basic + Dearness Allowance + Retaining Allowance, not on gross salary.

House Rent Allowance (HRA): Partially tax-exempt for employees paying rent, subject to conditions under Section 10(13A). The exemption is the minimum of:

- Actual HRA received

- 50% of basic salary (metro) or 40% (non-metro)

- Actual rent paid minus 10% of basic salary

This exemption is not available under the new tax regime.

Leave Travel Allowance (LTA): Tax-exempt if valid travel proofs are submitted for domestic travel within India, for 2 journeys within a block of 4 calendar years. Not available under the new tax regime.

Special Allowances: Fully taxable with no exemption benefits — typically used to fill out the CTC structure after other components are allocated.

Bonuses: Taxable, and may be governed by the Payment of Bonus Act for eligible employees earning up to ₹21,000/month. Minimum bonus is 8.33% of salary, capped at 20%.

Deductions

Provident Fund (PF): Employee contributes 12% of basic + DA; employer contributes 12% split into 3.67% EPF and 8.33% EPS. The wage ceiling is ₹15,000/month, and PF is mandatory for companies with 20 or more employees.

Employees' State Insurance (ESI): Employee contributes 0.75%, employer 3.25% — applicable only for employees with gross salary at or below ₹21,000/month. Mandatory for companies with 10 or more employees.

Professional Tax (PT): State-governed, typically ₹200–₹250/month, not applicable in all states. For example:

- Karnataka: ₹200/month for salaries ≥₹25,000

- Maharashtra: ₹200/month (₹300 in February) for males above ₹10,000; women earning up to ₹25,000 are exempt

- Tamil Nadu: Half-yearly slabs starting at ₹21,001/month

TDS: Calculated based on the employee's projected annual income, applicable tax regime (old vs. new), and investment declarations submitted at the start of the financial year. The new tax regime became the default from FY 2023-24; employees must explicitly opt out for old regime treatment.

26-Day vs. 30-Day Salary Calculation

For employees on monthly fixed salaries, most companies use 26 working days as the base (excluding Sundays) to calculate per-day salary for LOP deductions, though some organizations use 30 days. The method must be consistently applied per company policy and should be documented in the offer letter or HR policy.

New vs. Old Income Tax Regime

Under the new default regime, tax rates are lower but most exemptions (HRA, LTA, 80C deductions) are not available. Under the old regime, employees can claim exemptions but face higher base rates. Employers must compute TDS based on the regime chosen by each employee at the start of the year, so collecting regime declarations before the financial year begins is a non-negotiable payroll step.

Payroll Compliance in India: Key Laws and Obligations

Payroll compliance in India operates on two levels: central legislation (uniform across India) and state-level regulations (which vary significantly). Failing to follow either layer can result in penalties, audits, or reputational harm.

Central Compliance Obligations

Payment of Wages Act: Companies with under 1,000 employees must pay by the 7th of the following month; those with 1,000+ must pay by the 10th. On termination, wages must be paid within 2 working days.

Minimum Wages Act: State-governed minimum wages vary by industry and region. For example, Maharashtra Zone I unskilled wage is ₹13,635/month (July 2025), while Karnataka Zone 1 unskilled is ₹14,318.60/month (2024-25) — a gap of approximately ₹684 for comparable roles. Employers must ensure compliance with the applicable state minimum, not just a national figure.

EPF Act: Mandatory for companies with 20+ employees; contributions due by the 15th of the following month with monthly EPFO filings.

ESI Act: Mandatory for companies with 10+ employees; covers health and maternity benefits for eligible staff.

Payment of Gratuity Act: Employees with 5+ years of service are entitled to a lump-sum payout calculated at 15 days' wages per year of service, with a current cap of ₹20,00,000.

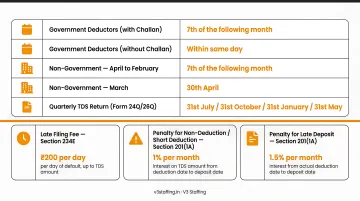

TDS Obligations

Employers must deduct TDS from salaries monthly under the Income Tax Act, deposit it by the 7th of the following month, file quarterly returns in Form 24Q, and issue Form 16 to all employees before June 15 after the financial year ends.

Penalties:

- Section 201(1A): 1% per month interest for late TDS deduction; 1.5% per month for late deposit

- Section 234E: ₹200/day for delayed TDS return filing, capped at the total TDS amount

State-Level Variability as a Compliance Challenge

State-level obligations introduce a layer of complexity that central laws alone don't capture. Key variables include:

- Professional Tax: Rates, thresholds, and filing frequencies differ by state

- Shops and Establishments Act: Working hours, leave entitlements, and overtime rules are state-specific

- Labour Welfare Fund (LWF): Contributions apply only in select states

- Multi-location operations: Businesses with teams across Hyderabad, Bengaluru, Chennai, Pune, Delhi NCR, and Mumbai must maintain separate compliance calendars per state

For enterprises and GCCs managing contract workforces across multiple states, payroll obligations for temporary employees carry distinct statutory risks — PF, ESI, TDS, and LWF filings all apply, and misclassification or missed deposits can trigger audits. Partnering with a staffing firm that holds statutory employer responsibility, like V3 Staffing, shifts that compliance burden and keeps filings consistent across every location.

Common Payroll Mistakes in India (and How to Avoid Them)

Operationally Costly Errors

- Calculate PF on basic + DA only — applying it to gross salary is one of the most common and easily avoidable errors

- Recalculate TDS when employees switch tax regimes or submit revised investment proofs mid-year, as stale figures cause over-deduction or under-deduction

- Apply state-specific rules for Professional Tax slabs and Shops & Establishments Act requirements rather than a single uniform deduction policy across all locations

Contractor Misclassification Risk

Engaging contract workers without correctly accounting for EPF, ESI, and TDS obligations can trigger retrospective demands and penalties from EPFO or labour enforcement authorities — particularly when a contractor's working arrangement closely resembles that of a full-time employee.

The Madras High Court (MRF Ltd case, 2025) clarified that if a contractor holds an independent PF code, the principal employer is not automatically liable without a Section 7A inquiry. For unregistered or non-compliant contractors, however, principal employers remain exposed to retrospective PF/ESI liability.

Record-Keeping Gap

Many companies process payroll correctly but fail to maintain adequate documentation — signed investment declarations, monthly payroll registers, proof of TDS deposits, ESI challans — which creates vulnerability during audits or employee disputes. Audit readiness requires documentation discipline throughout the year, not just at year-end.

Frequently Asked Questions

What are the basic steps in the India payroll process?

Payroll runs in three phases: pre-payroll (collecting employee data, attendance, and declarations), payroll calculation (computing gross salary and applying PF, ESI, PT, and TDS deductions to arrive at net pay), and post-payroll (disbursing salaries, filing statutory returns, and distributing payslips).

What is the payroll cycle in India?

Most Indian companies follow a monthly payroll cycle, with salaries typically processed in the last week of the month and credited by the last working day. The Payment of Wages Act mandates payment by the 7th or 10th of the following month depending on company size.

Is salary calculated 26 days or 30 days in India?

There is no single mandated rule. Most companies use 26 working days (excluding Sundays) as the base for per-day salary calculation for LOP purposes, while some use 30 days. The chosen method must be consistently documented in company policy.

What is CTC in India payroll?

CTC is Cost to Company — the total annual cost an employer bears for an employee, including basic salary, allowances, employer's PF and ESI contributions, gratuity accrual, and benefits. CTC is always higher than the employee's actual take-home (net) salary.

What are the types of payroll systems used in India?

Companies typically choose from three models: in-house payroll using spreadsheets or HRMS tools, dedicated payroll software for automated calculations and compliance filings, or outsourced payroll services where a third-party provider manages the full cycle. Outsourcing is especially common among GCCs and large enterprises.